Did the Truss-Kwarteng mini-Budget really cost the UK £74 bn? Truss not guilty says report

Did the Truss-Kwarteng mini-Budget really cost the UK £74bn? Truss not guilty says report

An alternative view of what tossed Truss from power last October

In this guest article for CIBUK.Org and Facts4EU.Org, an economist cries “foul”

In a strongly-worded rebuttal to the Remainer-Rejoiner chorus, written by economist Julian Jessop, he pours scorn on the guesswork of Establishment bodies, which we publish below.

“Speculation that Liz Truss is about to make a return to frontline politics has prompted a flurry of dodgy claims and daft statistics about the economic cost of last September’s mini-Budget”

– Economist Julian Jessop, 08 Feb 2023

Three headline figures used by her critics to ‘prove’ Ms Truss trashed the economy do nothing of the sort, argues Jessop. He then proceeds to tackle these allegations head-on in the demolition piece below.

Dodgy claims and daft statistics

A guest article by renowned independent economist Julian Jessop

Did the Truss/Kwarteng mini-Budget really cost the UK £ [insert huge number here] billion?

Let’s start with the biggest number: £74 billion

This figure (sometimes cited as £73 billion) appears to have been lifted from a headline in the Daily Express (26th October) which claimed that ‘Kwasi Kwarteng’s budget blunder cost UK an eye-watering £74 billion, finance chief reveals’.

Digging deeper, this was the Debt Management Office (DMO’s) estimate of the increase in the Net Financing Requirement for the fiscal year 2022-23 between April and September (actually £72.4 billion, but near enough).

© DMO 2023

CIBUK.Org found the document in question – click image to read it

This figure was included in the Growth Plan published on 23rd September, so was not news. In short, this was the extra money that the DMO expected to have to raise from the bond markets in 2022-23, relative to the projections in April.

Crucially, most of this figure was accounted for by the additional government support to help people and businesses with their energy bills. It also included the reversal of the 1.25% hikes in National Insurance contributions for both employees and employers.

It is therefore misleading to describe the ‘£74 billion’ (or whatever) as a cost to the UK. The implication is that the UK is somehow ‘£74 billion’ worse off as a result of policies adopted to prevent an energy crisis from becoming a catastrophe. This is clearly nonsense. I wonder also if those gleefully still retweeting this are happy to rely on one iffy headline in the Express.

There is another, only slightly smaller, number doing the rounds: £65 billion

This is the notional amount that the Bank of England said it was willing to commit to buy UK government bonds (aka ‘gilts’) to stabilise the market in the wake of the mini-Budget.

To recap, the rise in gilt yields was exacerbated by the increased use of liability-driven investment (LDI) strategies by some pension funds. This triggered a vicious spiral of margin calls and forced gilt sales, driving up yields further. The Bank of England (and other regulators) should have been on top of this much earlier.

Andrew Bailey

In the event, though, the Bank ‘only’ spent about £19 billion, on which it actually made a profit of about £4 billion. Claims that the mini-Budget “wiped £65 billion off the British economy in a month” are therefore nonsense too.

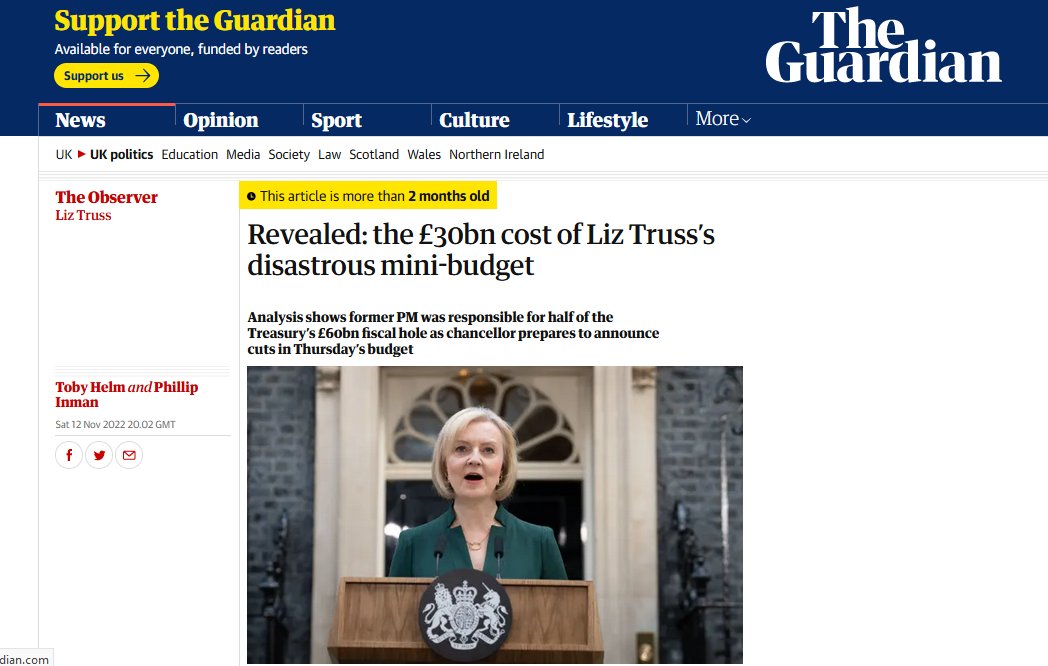

The third ‘zombie statistic’ is the smallest: £30 billion

This one appears to be based on a report in the Observer (12th November) which claimed that ‘Liz Truss’s disastrous mini-budget cost the country a staggering £30 billion’.

© The Observer

The £30 billion figure came from an (old) analysis by the Resolution Foundation (RF).

Around £20 billion of the £30 billion was simply a (high) estimate of the cost to the Treasury of those tax cuts in the mini-budget that have survived. This is mainly accounted for by the reversal of the increases in National Insurance (NI) contributions, and partly by the reductions in Stamp Duty.

Ironically, these measures were widely welcomed at the time, in part because they made a deep recession less likely. It is certainly odd to characterise £20 billion of tax cuts as a cost to taxpayers! The remaining £10 billion was an (old) RF estimate of the annual increase in the government’s cost of borrowing that might be attributed to the fallout from the Truss premiership. This is just speculation. Indeed, most market commentators would agree with me that any significant risk premia in UK assets have long since evaporated.

Of course, some will argue that even if the £74/65/30 billion figures are wrong, the mini-Budget ‘wrecked the economy’ (it didn’t) and that we are still paying the price now (we aren’t).

One example of this dubious narrative is the many tweets which blame the mini-Budget for the sustained increase in mortgage interest rates. But mortgage rates (and mortgage spreads) have also surged in many other countries, notably the US.

Another is the attempt to pin the IMF’s recent downgrade of the UK’s growth forecast for 2023 on ‘the country’s disastrous autumn of Trussonomics, which came too late for the IMF’s October forecasts’. This interpretation makes little sense.

In its October World Economic Outlook, the IMF itself noted that the fiscal expansion in the mini-Budget was ‘expected to lift growth somewhat above the forecast in the near term’, albeit at the cost of complicating the fight against inflation.

In fact, is it Jeremy Hunt who is to blame?

The new factor is therefore that Jeremy Hunt has tightened fiscal policy and signalled that the government will scale back its help with energy bills. This is a rather better explanation of why the IMF has downgraded its UK forecast for 2023.

In contrast, the forecasts for the euro area have been nudged up slightly, reflecting the announcements of additional fiscal support in the form of energy price caps and cash transfers.

Here, critics may respond that the reversal of policy in the UK was necessary to restore credibility in the financial markets after the botched implementation of Trussonomics, and that interest rates are still higher than they would otherwise have been.

However there is actually very little evidence to support this. In any event, it should have been sufficient for a new Chancellor to cancel the surprise measures that most unsettled investors – notably the additional cuts in personal taxes. Instead, the pendulum appears to have swung too far the other way.

History is often written by the victors. However, it is utterly bizarre to blame a forecast revision which is mainly due to tighter fiscal policy and expectations of still-high energy prices on a plan to cut taxes and provide more support with energy bills.

– By Julian Jessop, 09 Feb 2023

For Rejoiners who ask “Who is Julian Jessop?”, try this

Julian is a professional economist with 35 years of experience gained in the public sector, the City and consultancy, including stints at HM Treasury, HSBC, Standard Chartered Bank and Capital Economics. He was previously Chief Economist at the Institute of Economic Affairs. Having left in 2018 he is still an IEA Economics Fellow, a member of the IEA’s Academic Advisory Council, and sits on the IEA’s Shadow Monetary Policy Committee (SMPC).

He was a Director, Chief Global Economist, and Head of Commodities Research at the leading independent consultancy, Capital Economics, and was also a leading member of the Capital Economics team, headed by Roger Bootle, which won the £250,000 Wolfson Economics Prize in 2012 (for the best plan to break up the euro).

Julian has provided expert testimony to many parliamentary select committees, on topics including the economic outlook, fiscal policy, the cost of living, international trade and Brexit, and has advised the OBR.

He graduated with a first class honours degree in Economics from Cambridge and has further qualifications both in economics (an MPhil, also from Cambridge) and in law (the post-graduate diploma from the College of Law, gained when he was Head of Economics at what was then the Lord Chancellor’s Department).

We would say this is a pretty impressive CV. Julian is financially independent and free to speak his mind, which he has done in his article above.

Observations

CIBUK.Org tries to bring readers stimulating information that is rarely seen in the mainstream media. In this way we aim to broaden the public debate on key issues which affect them. Please, please support us with a donation today so that we can keep going.

To read more great articles like this (no paywall),

see our news page and rebuttal articles page!

And please help us to carry on!

Whether the presentation of the mini-budget was ill-prepared or not (it was), the fundamentals behind the economic policies of the short-lived Truss administration are now beginning to be seen as sound.

In his article, economist Julian Jessop points out just three examples of the ludicrous ‘forecasts’ from the Establishment which had clearly set out to get her. He also shows how events were in train well before the Truss-Kwarteng mini-budget and that the IMF’s latest downgrade in the UK’s growth forecast has nothing to do with Ms Truss but rather more to do with the new PM Rishi Sunak and the new Chancellor Jeremy Hunt.

We remain non-partisan and make no case for any particular politician over another. What we can say, however, is that there was a clear attempt to sabotage Ms Truss’s premiership with fake news.

We are grateful to Julian Jessop for permission to use his research.

Main image: montage © CIBUK.Org

This report has been co-published with our affiliated organisation, Brexit Facts4EU.Org.